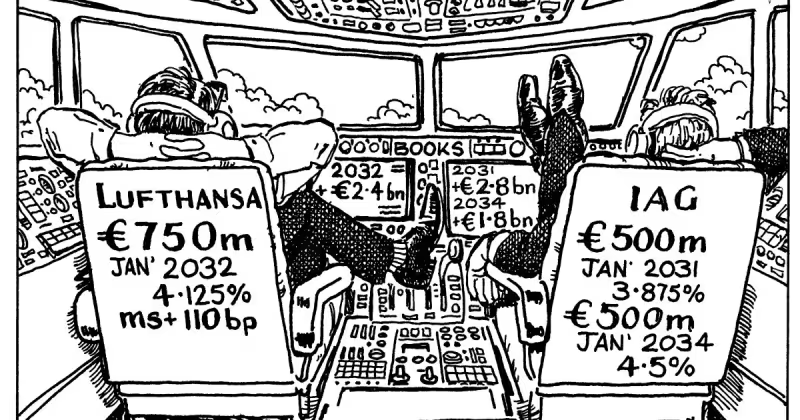

Lufthansa Group is preparing a new eurobond offering and is reportedly considering senior unsecured debt with a maturity of about 5.7 years, while conducting investor calls to gauge demand before deciding whether to go ahead.

The maturity under discussion — roughly 5.7 years — and the fact that the company is actively testing the market with investor calls are the clearest signals yet that Lufthansa is weighing a multi‑hundred‑million to multi‑billion euro debt move to shore up funding options; the total amount to be raised has not been disclosed.

The talks come as airlines face a renewed cost squeeze. Jet fuel, one of the largest expenses for carriers and second only to labor costs, has risen, adding direct pressure to operating margins. Debt markets remain a key route for airlines to refinance obligations, support fleet investments or preserve balance‑sheet stability, and the planned transaction would, if completed, further reinforce Lufthansa’s access to international capital markets.

For now the debate inside the company appears pragmatic: investor calls are designed to measure appetite and pricing tolerance before any launch. Lufthansa has a track record of returning to bond markets and other financing instruments since the pandemic to support liquidity and strategic investments, a pattern that underpins why management would test the eurobond route rather than rely solely on bank lines or other measures.

That testing matters because the backdrop is mixed. On the revenue side, Lufthansa has been benefiting from robust premium travel demand, growing transatlantic traffic and improved yields on many long‑haul routes, a dynamic that has helped restore profitability after the pandemic. On the cost side, however, climbing jet fuel and broader inflation, higher airport charges, environmental compliance costs and supply‑chain constraints for aircraft deliveries and maintenance are squeezing margins across European carriers.

The tension is straightforward: stronger high‑yield demand and recovering long‑haul performance give Lufthansa a commercial case for fresh financing to invest in its fleet and operations, but rising input costs make the timing and size of a bond sale more sensitive to market conditions. If investor interest is tepid or pricing unattractive, the company may choose to delay or scale the deal. Conversely, healthy demand would enable Lufthansa to lock in medium‑term funding while markets remain open.

For investors and competitors the immediate question is liquidity management. Airlines across Europe are already navigating inflation, airport fees and environmental rules alongside logistics challenges. A successful eurobond would provide Lufthansa with an additional tool to refinance existing obligations and to support strategic investments without immediately tapping more expensive or dilutive options.

Decisionmaking now rests on the investor calls and the trajectory of costs such as jet fuel. If market appetite proves sufficient, the offering is likely to proceed and will strengthen Lufthansa’s standing in international capital markets; if not, the company will probably pause and look to alternative financing channels it has used since the pandemic. Either way, the outcome will shape how aggressively Lufthansa can pursue fleet and network plans while balancing a tougher cost environment.